Phil Fersht at HFS Research coined the term Services-as-Software (SaS) to describe what happens when people-based work blurs with technology to the point where the line between a service and a software product disappears.

Nasscom frames it as the shift from fragmented service and software silos into a unified, AI-powered model where success is measured not by uptime or ticket resolution, but by business outcomes and P&L impact. HFS surveyed over 600 enterprise decision-makers and found more than two-thirds are frustrated with both their software and services investments and are actively looking to renegotiate.

Both bodies are describing a delivery transformation. What neither of them tells you is what happens to your commercial story when that transformation occurs inside your own firm.

That’s the conversation most IT services founders aren’t having. And the silence is expensive.

The Split Is Already Happening

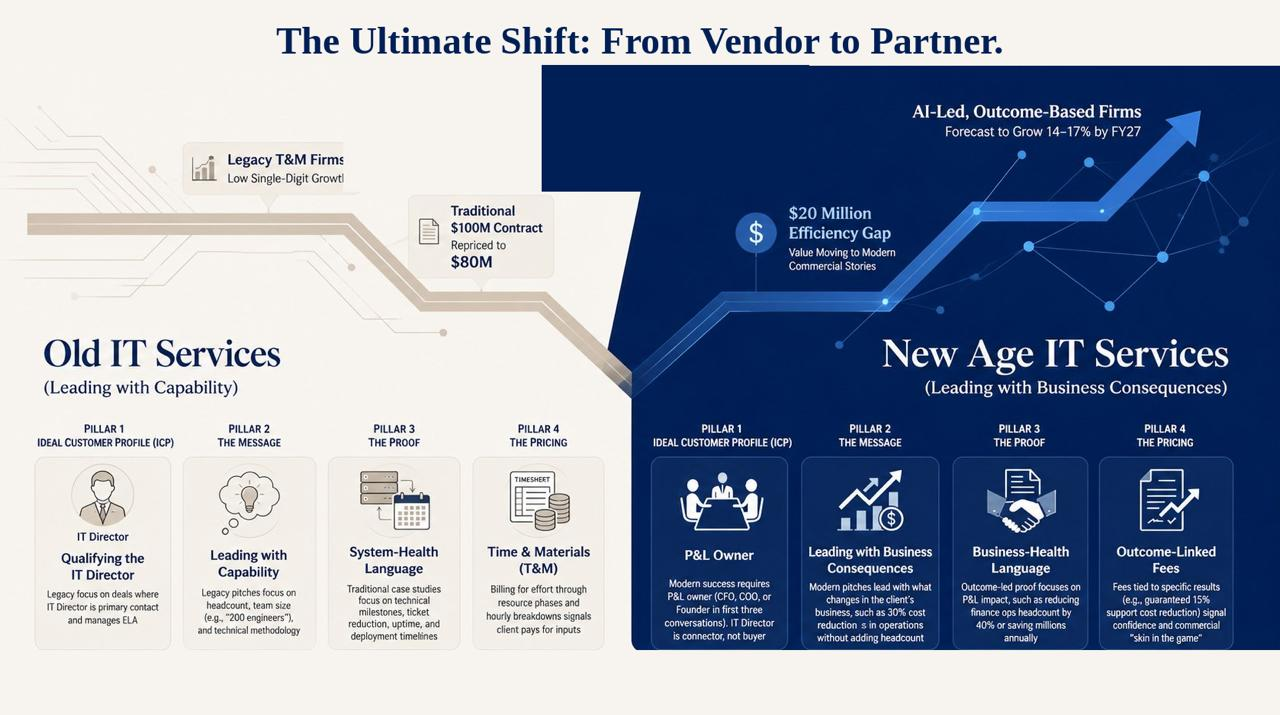

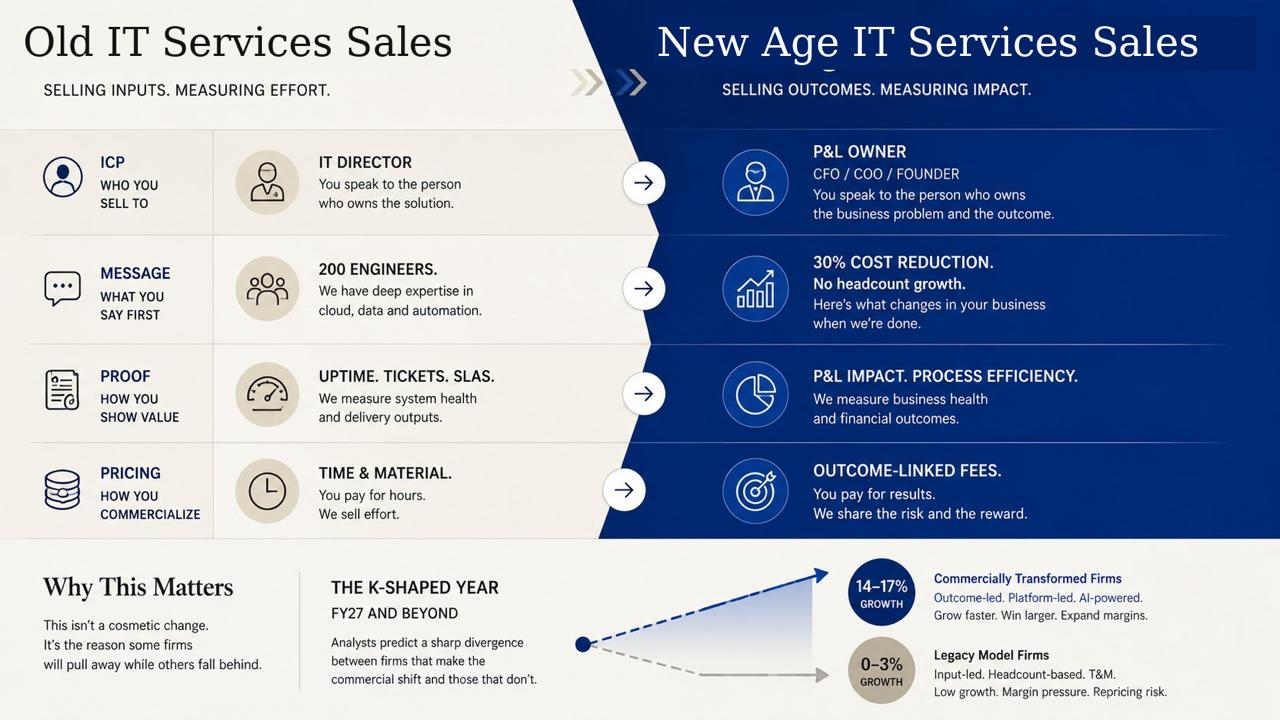

Analysts at Forrester and UnearthInsight have started calling FY27 a K-shaped year for IT services. Firms moving toward AI-led delivery and outcome-based contracts are expected to grow at 14 to 17 percent. Firms still running on legacy time-and-material models are forecast to grow at low single digits, if at all.

That divergence isn’t a technology story. Both groups have access to the same AI tools. Both have engineers who’ve run pilots, deployed agents, and built automation layers. The difference is commercial. One group changed what they promised in the room. The other changed what they delivered in the building and left the pitch untouched.

I keep seeing the same pattern in conversations with founders. They know exactly what their firm does now. Ask them in a coffee conversation and they describe it clearly — outcomes guaranteed, AI handling tier-one work, faster delivery, measurable business impact. Then you look at their last proposal. It reads like a staffing plan with a tech glossary attached.

What Actually Changed in Delivery

At some point in the last two years, most IT services firms quietly rebuilt how they work. Not by announcement. Not with a press release. Just operationally — fewer junior resources on standard tasks, AI agents handling work that used to go to a team of three, delivery timelines compressing from months to weeks on the same scope.

A 2025 study by Nasscom and EY examined 1,200 tasks across IT services and BPO and found AI can deliver productivity gains of 40 to 80 percent at the task level. EY India’s technology sector leader called this “the biggest operating model rewrite since offshoring.” Those gains are real and already embedded in how the better firms deliver.

But the commercial story most firms are telling in sales conversations is still built around the old model:

- The pitch opens with team structure and methodology

- Case studies lead with deployment timelines and engineer headcount

- Proposals break down into phases, resources, and hours

The delivery model changed. The sales story didn’t. And that gap — that specific, quiet, unglamorous gap — is where deals are dying.

HFS Research projects this shift will become a $1.5 trillion market by 2035, absorbing revenue from traditional IT services and SaaS alike. For firms on the wrong side of it, the erosion is already visible in contract values. Yesterday’s $100 million IT services contract is now worth $80 million — the $20 million gap absorbed by AI-led efficiency. That money hasn’t left the industry. It’s moved to firms who changed what they say before the work begins.

Sources: HFS Research, February 2025; Nasscom/EY, 2025; Business Standard earnings analysis, 2025

You’ve Changed What You Deliver. You Haven’t Changed How You Sell It.

Where the Mismatch Shows Up

Clients who’ve started to understand what AI-led delivery actually looks like — and more of them have than founders realise — read a T&M proposal and draw a specific conclusion: this firm is charging for human effort that AI is now doing. They’re right.

Which is why deal tenures across the sector are shortening by 15 to 30 percent, with buyers unwilling to lock into long-term contracts on a model they know is being repriced underneath them.

The mismatch shows up in three specific places. Repricing alone doesn’t fix all three:

| Where It Breaks | What’s Happening | What the Buyer Concludes |

| Proof | Case studies still measure team size, deployment speed, and technical milestones | This firm is selling me the old model |

| Buyer | Still pitching IT leadership — the person who used to sign, not the one who does now | This is a vendor, not a partner |

| Pricing structure | T&M billing signals effort, not outcome | They charge for hours. I’m paying for results I can’t see yet. |

There’s a language problem underneath all three.

Most IT services case studies are written in system-health language — uptime, tickets closed, engineers deployed. That language hits the IT Director’s inbox and stops there. Whoever now controls the budget — a dedicated CFO, a COO, or a founder carrying both roles — is reading for business-health language: cost impact, process efficiency, P&L outcome. If your proof doesn’t speak that language, it doesn’t reach the person who signs.

The buyer, whether that’s a standalone CFO, a COO, or a startup founder running the whole P&L, isn’t evaluating your technical capability. They’re asking one question: what changes in my business when this engagement is over? If your pitch doesn’t answer that in the first ten minutes, it doesn’t recover.

Two Firms. Same Industry. Different Revenue Outcomes.

The clearest proof that this is a commercial story problem, not a technology problem, is playing out right now inside the IT services sector. HFS Research identified a group of mid-tier providers that are actively delinking revenue and margin from headcount. The contrast with the industry average is sharp.

| Criteria | Breakout Mid-Tier (Persistent, Coforge) | Lagging Large-Cap (Cognizant, Capgemini) |

| Revenue growth Q1 FY26 | ~20% YoY | ~1.5% YoY average |

| Commercial positioning | Revenue-generating transformation | Legacy cost-reduction narrative |

| Deal structure | Outcome-linked, platform-first | T&M, headcount-based |

| Market valuation signal | Premium to revenue | Below annual revenue |

| What changed first | The commercial story | The delivery capability |

Sources: HFS Research, October 2025; UBS Q4 FY26 IT sector analysis; service provider earnings reports

Same industry. Same AI tools available to both groups. Same enterprise clients being pursued.

Persistent repositioned its commercial story around revenue-generating transformations, not cost-saving operations. That’s a message change, not a delivery change. It shifts what they open with, what they propose, and what the client is buying into when they sign. Coforge rebuilt its engagement model around platform-led outcomes rather than resource deployment. The revenue followed the story, not the other way around.

Cognizant and Capgemini, both with enormous delivery capabilities and substantial AI tooling — now trade at market valuations below their annual revenues. Analysts aren’t pricing in delivery risk. They’re pricing in commercial model risk. The concern isn’t that these firms can’t deliver the new model. It’s that their sales story, contract structure, and positioning haven’t moved fast enough to reflect what the firm actually is.

What specifically Persistent changed in its client conversations, what exact words shifted, which stories they stopped telling, how they restructured the first meeting — isn’t published anywhere. But the revenue gap is clear enough to read something from it.

What Needs to Change — In This Order

The delivery model is not the problem. Most IT services firms reading this are already delivering something meaningfully different from what they pitched three years ago. The commercial story is where the work is. And the order matters — because you can’t write the right message until you know who you’re writing it for, and you can’t build the right proof until you know what that buyer cares about.

1. ICP — Redraw Who You’re Selling To

The buyer has moved. Not to a new job title — to a different problem. Whether your client is a large enterprise or a founder-led business, the person who now controls the decision isn’t the one managing your SLA. It’s whoever owns the P&L.

In a larger organisation, that’s typically a dedicated CFO or COO. In a fast-scaling startup — which is where a significant slice of IT services deals happen — it’s often the founder themselves, carrying the CTO, operations, and budget-holder roles simultaneously. The title changes. The question doesn’t: what changes in my business when this engagement is over?

If your qualification criteria still filter for IT director first, you’re starting every deal in the wrong room — whether that room is in a corporate tower or a Series B startup’s open-plan office.

| Before | After |

| Qualify deals where the IT Director is engaged. Present proposal after demo. | No qualified deal unless the person who owns the P&L is in the first three conversations, whether that’s a standalone CFO, a COO, or a founder carrying all three roles. The IT Director is a connector, not a buyer. |

The pipeline problem most founders are feeling right now has its roots here, not in the message, not in pricing. You’re having the right conversation with the wrong person. The IT director will nod. The deal will stall. And you’ll spend another quarter wondering what happened.

2. Messaging — Lead With the Consequence, Not the Capability

Once you’re in the right room, the first sentence determines whether the conversation continues as a peer discussion or a vendor pitch. Most IT services firms open with capability. The person who owns the P&L — whether that’s a CFO, COO, or a founder running the whole show — doesn’t care about capability. They care about what changes in their business when the engagement is over.

| Before | After |

| We have 200 engineers with deep expertise in cloud and automation. | We have reduced IT operations costs by 30% in 18 months without adding headcount. |

The second version doesn’t mention your team size, your methodology, or your technology stack. It names a result that exists in the buyer’s world. That’s the conversation opener that earns the next hour.

3. Proof — Rewrite the Case Study

Your best case studies are probably working against you. They’re full of system-health language — team size, uptime percentages, delivery timelines, technical milestones. These were the right signals for the IT director. The person who now controls the budget — a founder, a CFO, a COO, or all three rolled into one — is reading business-health language: what changed in our cost structure, what improved in our process efficiency, what was the P&L impact.

| Before | After |

| Deployed 12 engineers over 6 months. Delivered on time and on budget. | Reduced client’s finance ops headcount by 40%, saving $2.4M annually. Transition completed in 14 weeks. |

Same client. Same engagement. Completely different story. And here’s what most founders miss: rewriting the case study isn’t just a marketing exercise. It’s a qualification tool. The right buyer reads the second version and leans in. The wrong buyer scrolls past it. Both outcomes are useful.

4. Pricing — Let the Story Come First

How you structure the contract communicates what kind of firm you are before you’ve said a word about delivery. T&M says: we charge for effort. Outcome-linked structure says: we charge for results, and we’re confident enough in what we deliver to build the contract that way.

| Before | After |

| Phase 1: Discovery — 3 resources, 400 hours, $60K. Phase 2: Build — 8 resources, 800 hours, $120K… | We guarantee 35% reduction in your tier-1 IT support costs within 90 days. If we miss that number, the success fee doesn’t apply. |

The second version isn’t just a pricing model — it’s a positioning signal. It tells the buyer this firm has enough conviction to put commercial skin in the game. Firms that move to outcome-based pricing without changing the commercial story first find buyers don’t trust the model, because the positioning hasn’t earned it yet. Story first. Pricing follows.

The Real Divide Isn’t Technology

The IT services sector has been through one operating model rewrite before. Offshoring.

The firms that caught the commercial wave early built the industry’s biggest success stories. The ones that were late spent years catching up on terms their competitors had already set.

The K-shaped year analysts are predicting for FY27 is the same pattern. And the dividing line isn’t who has the better AI stack. It’s who rebuilt the commercial story first.

So here’s the question worth sitting with. If you removed all the technology language from your last three client proposals — every reference to AI, automation, platforms, and deployment — what’s left?

Is the story that remains the reason your best new clients are actually hiring you?

Or is it the story you’ve always told, dressed up in newer vocabulary?

Key Takeaways

- AI-led delivery is already changing the economics of IT services.

- The biggest gap isn’t operational. It’s commercial positioning.

- P&L owners now drive buying decisions, not just IT leadership.

- Outcome-based messaging converts better than capability-led positioning.

- Case studies must shift from technical proof to business impact proof.

- Pricing structure signals confidence in outcomes, not effort.

- The firms winning this transition changed their commercial story before their competitors did.

Sources and Citations

- HFS Research

- Nasscom & EY AI Productivity Study, 2025

- Forrester Research

- UBS IT Sector Analysis, FY26

- Business Standard Earnings Analysis, 2025